Accrual Concept In Accounting

T R Y Accrual Concept Accrual Definition An Facebook

Accrual Concept

Accounting Concepts Accrual Accounting

Accrual Concept

Accrual Concepts Of Accounting Definition Explanation Example And Importance Accounting For Management

Accrual Accounting Concepts Financial Accounting Lecture Slides Docsity

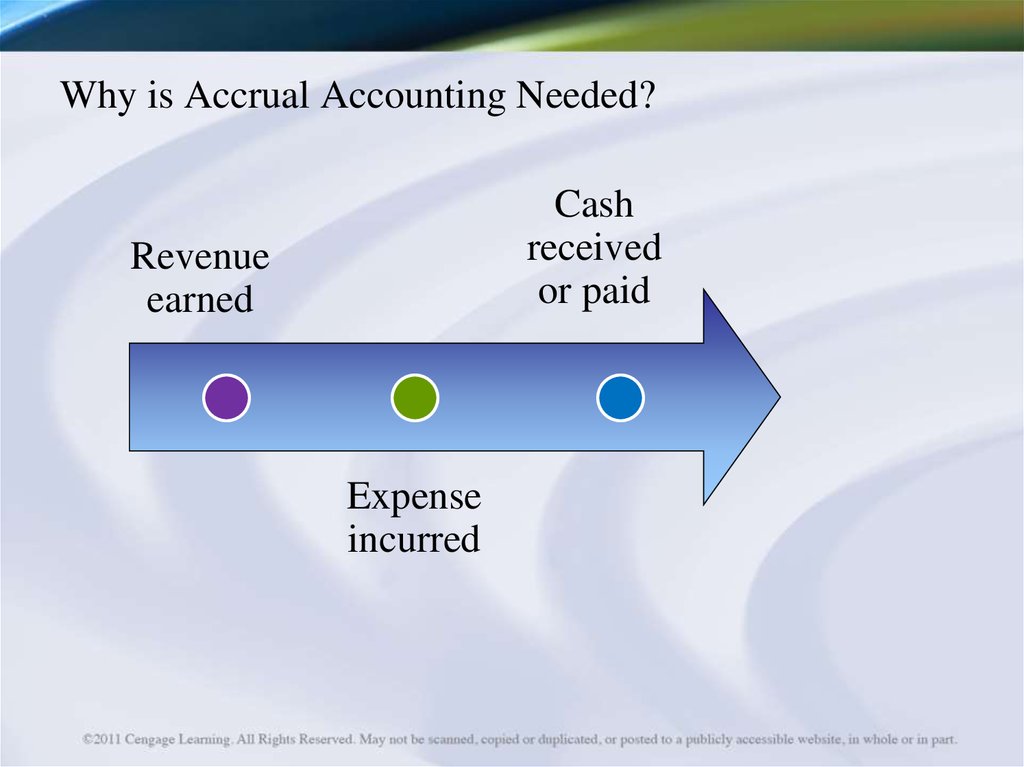

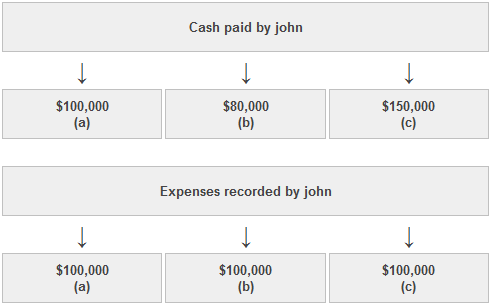

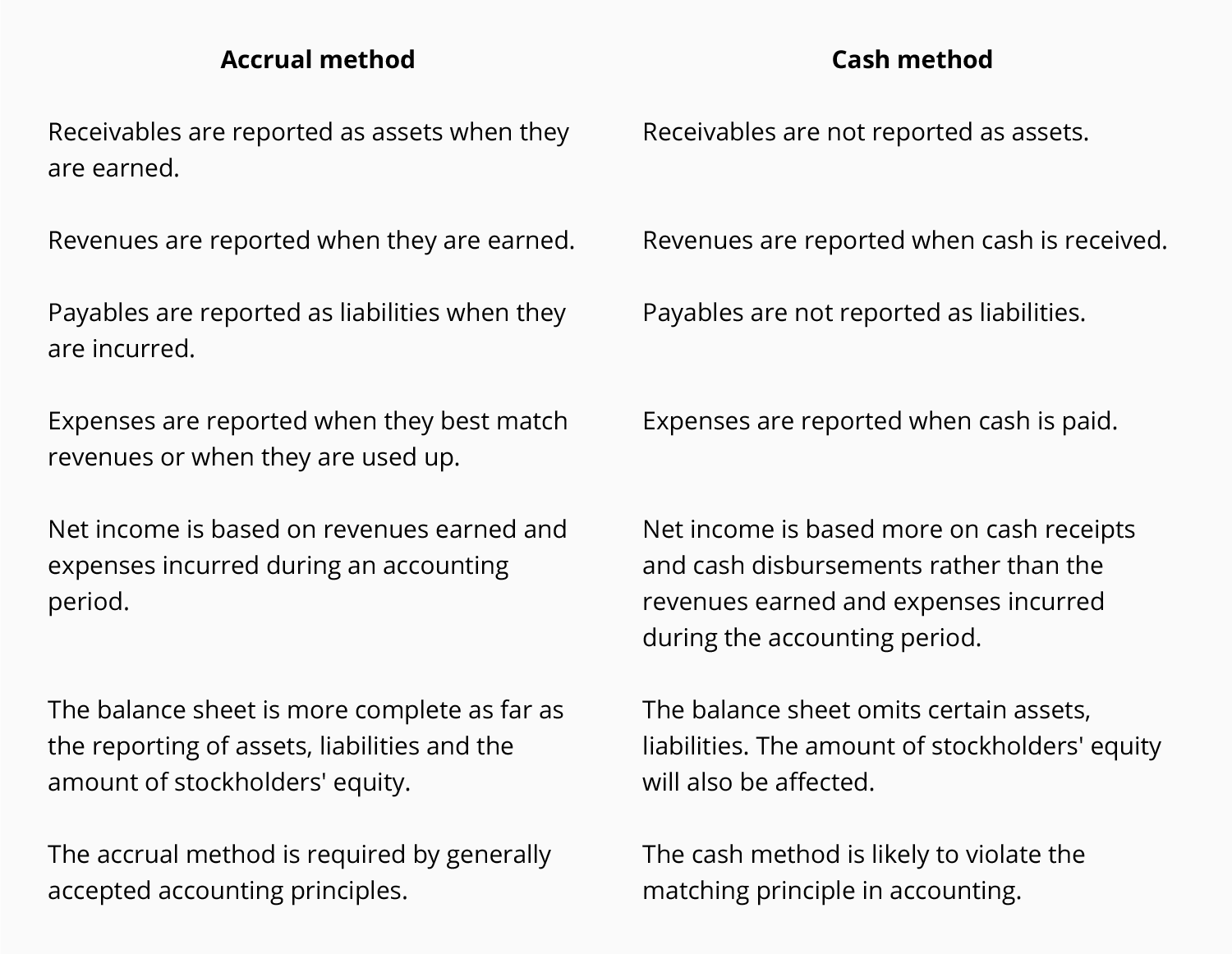

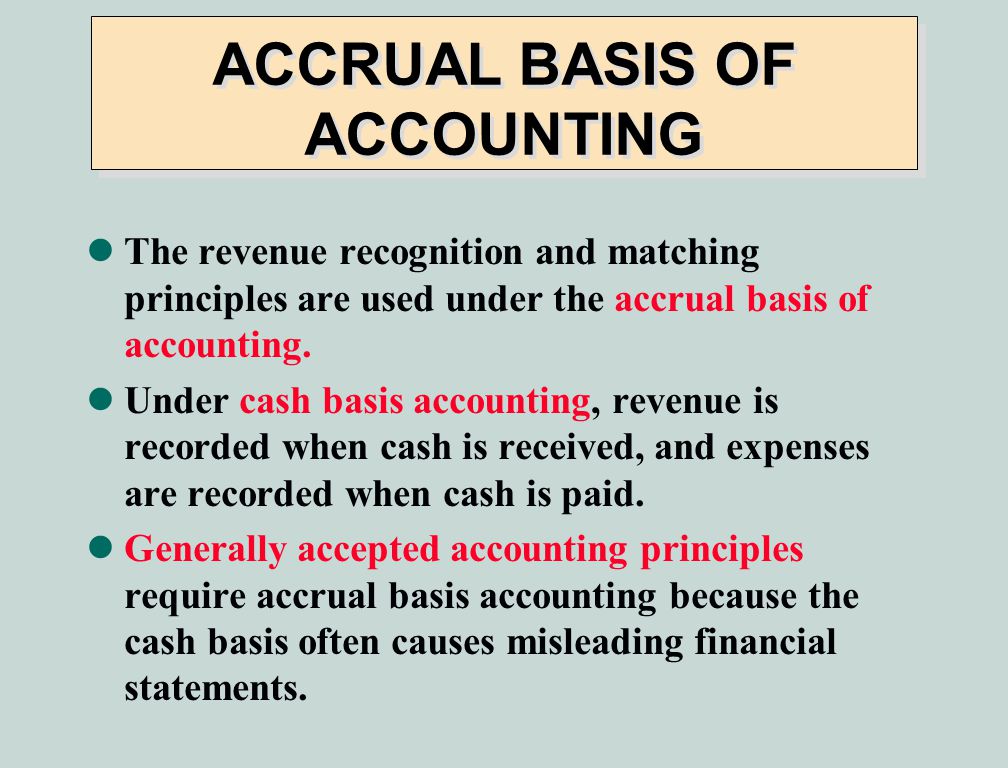

In the accrual accounting method the revenue is recognized on the day it is earned and the expenses are recorded on the date they are incurred.

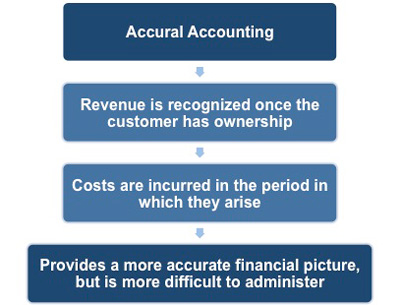

Accrual concept in accounting. On the other hand expenses are recognized when they occur no matter payment is paid or not. This accrual accounting guide teaches business owners what they need to understand and how to use accrual accounting effectively. Accrual concept is one of the basic accounting principle and is followed all over the world. In simple terms it is the accounting adjustment of accumulated debits and credits.

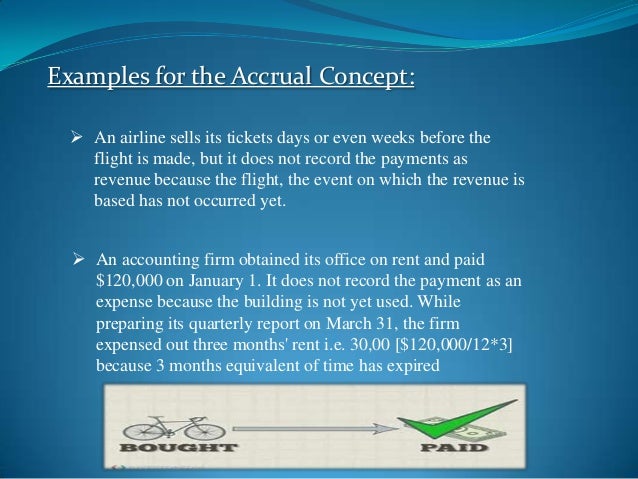

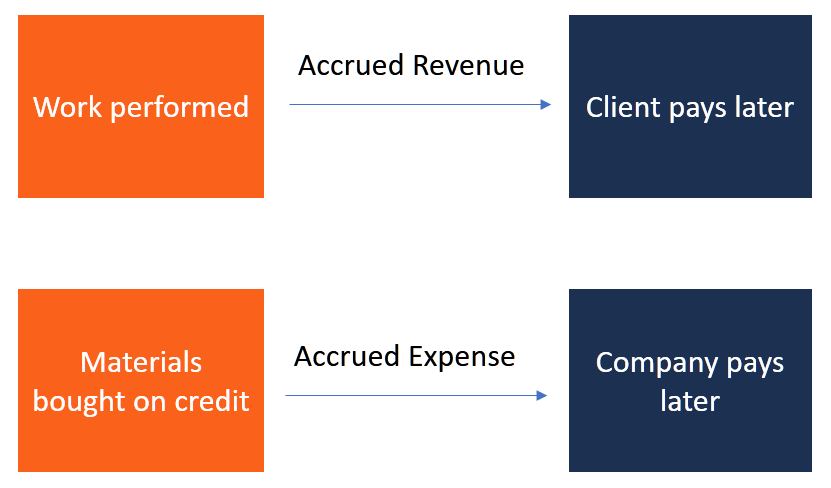

Accruals concept is therefore very similar to the matching principle. Accrual concept is the most fundamental principle of accounting which requires recording revenues when they are earned and not when they are received in cash and recording expenses when they are incurred and not when they are paid. Or accrual accounting accruals refer to the recording of revenues that a company has earned but has yet to receive payment for and the expenses that have been incurred but that the company has yet to pay. Accrual definition an accrual is a journal entry that is used to recognize revenues and expenses that have been earned or consumed respectively and for which the related cash amounts have not yet been received or paid out.

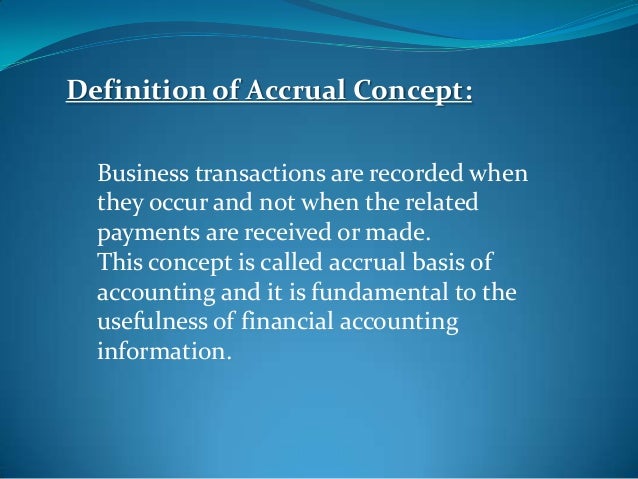

According to this principle revenues should be recognized when they are earned no matter payment is received or not. Accounting experts share basic definitions and concepts formulas examples sample journal entries and advice to help best account for revenue. As per this concept the effect of transactions and other events are recognised as and when they occur and not when cash or cash equivalent is received or paid and they are recorded in the transactions records and reported in the financial statements of the period to which they relate. Accrual concept or accrual basis of accounting is the method of accounting which involves recording the accounting entries in the books of accounts when the revenues expenses becomes accrue due and not when the money against such revenues expenses are received paid respectively.

Accrual concept of accounting requires that financial statements reflect transactions at the time when they actually occur not necessarily when cash changes the hands. Gaap allows preparation of financial statements on accrual basis only and not on cash basis. The recognition of revenue and expenses is not concerned with the dates of actual cash flows.

Ppt Chapter 4 Accrual Accounting Concepts Powerpoint Presentation Free Download Id 6430967

Accrual Accounting Guide To Accruing Revenues Expenses

What Is The Accruals And Matching Concept Youtube

What Is Accrual Concept Accounting Concepts Principles Conventions Ca Cpt Cs Cma Youtube

Accounting Principles Accrual Accounting Principle

Accrual Concept

Bookkeeping Accrual Method Accountingcoach

Accounting Accounting Concepts Accrual And Matching Concept Important For Ugc Net Upsc Cse Ssc Flexiprep

Overview Accrual Accounting Revenue Recognition Matching Principle Intro To Accounting

Accrual Concept And Realisation Concept Hindi Nta Ugc Net Accounting Principles Accounting Standards With Mcqs Unacademy

Chapter 6 Accruals And Prepayments

Accrual Concept

Apply Matching Concept Step By Step Understand Meaning Purpose